To PMs: What do you think about BNPL?

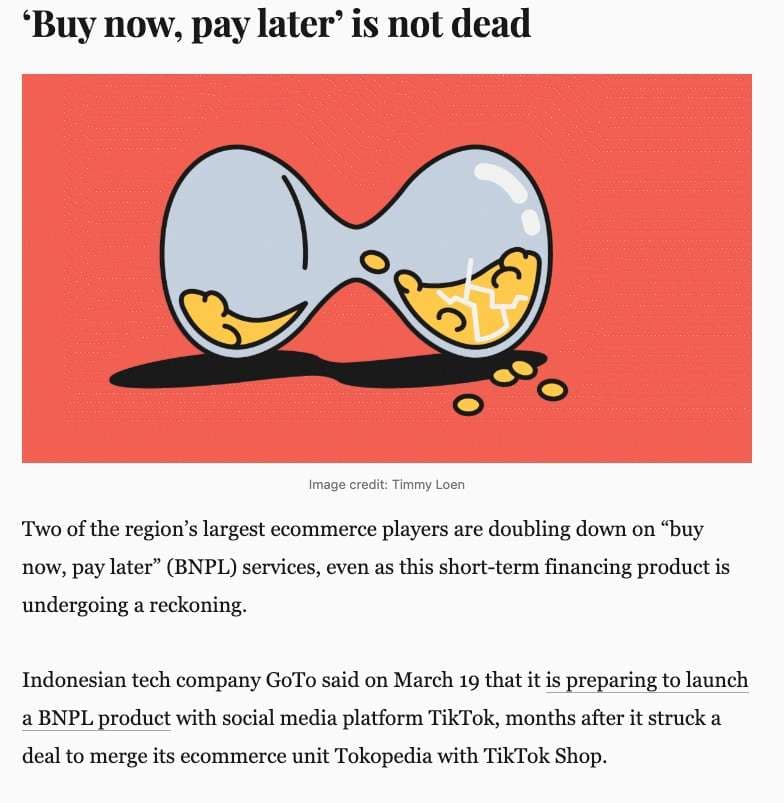

GoTo is going to launch a BNPL product with TikTok soon. As a PM what are some things that you would do for something like this to succeed?

BNPL is inherently loss making, you need a 70:30 mix of interest players and zero interest players to be profitable. The dominance of CC and no perceived monetary benefit to users will limit its growth.

@I_dont_know_how_to_ It makes a ton of sense tbh. BNPL can only work if cost of capital is super low imho. I wonder how will GoTo manage this tbh.

What would you do to make it super successful?

It's been cracked by Bajaj finance, in the offline segment especially in the furniture market. You offer zero cost with some shaddy charges.

BNPL is literally the definition of a loan. Jokes aside, lending is not a distribution business, it’s a collection business. Unless the collection of outstanding dues is fixed, I don’t see anything succeeding.

@holdencaulfield Very true actually. As a PM what would you focus on?

How are you assessing the BNPL limit to begin with? That will restrict your NPA losses.

What is the payment policy and late payment charges? I once got late payment charges waived off just by calling customer care.

At the end of the day, the more partnerships you do, better are the chances of growth, so integration SDK and third party onboarding should be super easy with great CX.

Cashback on BNPL usage can be a big play here to improve adoption but I have seen customers getting more attracted to upfront discounts in India atleast.

Personally I don't use any BNPL app since at the end of the day, it is a personal loan and I don't want to have a loan against my name every month in CIBIL books.

I also feel it is a loan trap for innocent folks like college students, low wage workers.

There’s a large population in south east Asia which is out of credit bureau records and financially illiterate at the same time. Though the margins for an intermediary providing BNPL are low, aggressive dark patterns can fetch you money if done right. The possibility of coupling user growth with one NBFC/ financial house and using it to drive more partnerships and hence more loaded loan books seems to be the play. I’m not from finance so can’t comment on what it’d mean over a longer period of time

@Dihaadi You are hinting at something that not many will realize. It is a ploy to disburse as many loans as possible to acquire users today in hope of future demand.

I was really interested in trying bnpl but the rate of interest always put me off.

If i can afford a product, bnpl doesn't make sense because I'm paying extra money for the same product.

If i can't afford a product, bnpl still doesn't make sense because I probably shouldn't be buying it in the first place if i can't afford it. Financing options with banks are anyways better than fintech, might as well get personal loan or credit card for purchases instead.

@Fawkes This makes so much sense man.

The lending partners behind the some of the apps are scam companies. Worst customer support, reporting false information to CIBIL , and leaking personal data. Better to avoid bnpl apps or do good research on their lending partners.

@iOSdev It actually makes a ton of sense. Klarna and AfterPay and Affirm have done super well.

On a personal level, I don’t believe in BNPL. But I have a certain background, upbringing and privilege that puts me in that position. But given the recent data I read about it. I believe it has potential, imagine no low net worth individuals with SMEs getting access to credit at reasonable prices. They could use that money to grow their business (Too the liberty to add loans to BNPL) because BNPL is essentially being used to onboard customers to credit, monitor their credit behaviour (CIBIL etc) to provide them access to credit.

https://www.transunion.com/lp/empowering-credit-inclusion-global-research

Interesting read if you are curious to understand it a bit more.

With BNPL , customer retention becomes very tough because if a consumer is getting access to any product which is somewhat good , there are higher chances that he will look for something better in the same domain

- onboarding the customers via subscription based model or buy then use allows the companies to experiment with the features while customer is arrived at the platform till the next renewal but that's not the good case with BNPL

-ARR gets drop by a greater percentage as new users don't add any value until or unless they're coming back to products due to some USP

@IamBiztech Smart. Yes.

except life saving bare necessities, any person who indulges in this BNPL is the biggest fool of 21st century.

The mix needed for interest paying users in a BNPL portfolio has not been achieved yet by any growing economy, I don’t see why this would be any different.

BNPL can be a hook to get users in and then create personal loan, co branded credit card products based on user data etc. However, it is still not clear how an org burning money on BNPL can make so much profit through unsecured lending that overall profitability can be achieved.

One model that can work is if BNPL gets massive distribution so much so that you start seeing it across all large ticket purchases where you’re able to charge partners, I don’t see how this can become profitable.